2026 Fringe Benefits Tax Update

The Fringe Benefits Tax Year End is Fast Approaching

Fringe Benefits Tax (FBT) continues to attract close attention from the ATO, particularly where common employee benefits are involved. As the FBT year from 1 April 2025 to 31 March 2026 comes to a close, the focus is not on new rules or higher tax rates. Instead, it is on whether businesses are properly identifying, recording and reporting the benefits they provide. Most FBT issues arise from assumptions carried over from previous years or gaps in record keeping, rather than deliberate non‑compliance.

This FMA Insights covers:

Key dates and deadlines

FBT rate comparison

What businesses should be doing before 31 March 2026

What’s changed for FBT in 2026 and what the ATO is focusing on

This update outlines the key FBT issues for business owners, the areas attracting the most ATO attention, and the practical steps you should be taking now to reduce risk and stay compliant.

Key Dates

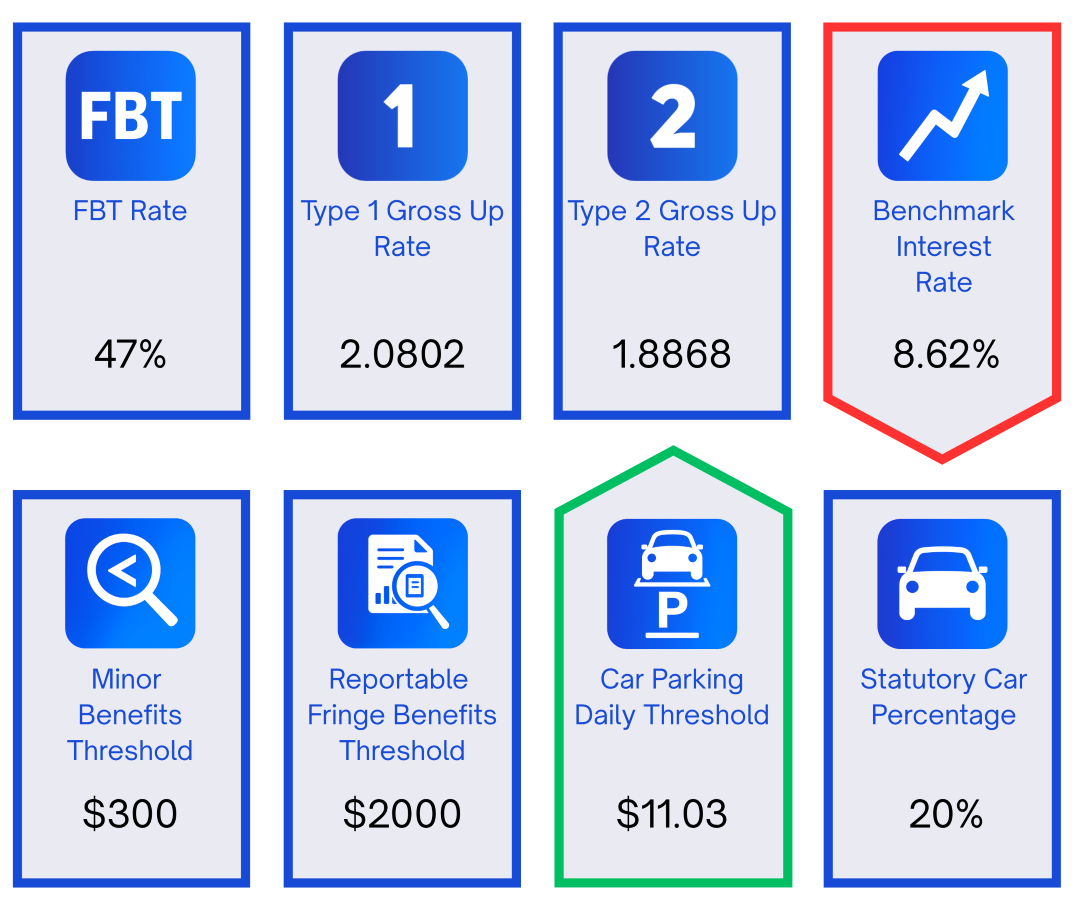

2026 FBT Rates

What Businesses Should Do Now Before 31 March 2026

Before 31 March 2026, there are some critical actions businesses must complete to meet their FBT compliance obligations.

Completing the following items before year end will help ensure your FBT position is accurate, supportable, and audit‑ready.

-

For every employer‑provided vehicle, employers must ensure employees do the following:

Take a clear photo of the vehicle’s odometer showing the reading as at 31 March 2026.

Email the photo to a centralised contact, confirming in writing that the photo of the odometer relates to the relevant vehicle and referencing the vehicle number plate.

Employers must retain this evidence, as the ATO treats odometer records as a core FBT compliance requirement.

-

Where employee contributions are being used to reduce FBT:

Contributions must be actually paid on after tax income by 31 March 2026, or

Properly documented where they are applied under a valid set‑off arrangement or written agreement, such as a salary sacrifice arrangement.

Please contact us if you require assistance with calculating, documenting, or finalising any employee contributions.

-

Before 31 March, you should confirm with your employee:

Whether the vehicle qualifies for any exemptions, noting that employee declarations must be completed for any utility vehicle exemptions.

(Any declaration can be finalised prior to the FBT return being lodged.)That any logbooks are valid, current, and accurately maintained.

That all private use of the vehicle has been correctly identified and accounted for.

Incorrect assumptions around vehicle use and exemptions remain a major ATO focus area.

-

By 31 March, you should ensure all required FBT records are complete and readily available, including:

Receipts and invoices

Logbooks and odometer records

Approved alternative records

Documentation supporting any exemptions applied

Provide employees with required declarations

(These can be executed up to the due date of the return)

Missing or incomplete records significantly increase the risk of ATO review and audit.

What Businesses Should Do Differently in 2026?

Compared to previous years, businesses should take the time to revisit their vehicle arrangements, particularly any plug-in hybrid electric vehicles (PHEVS), review how FBT records are being kept, make sure entertainment is treated consistently across tax, GST and FBT, confirm employee contributions are properly documented, and carry out an annual FBT review even if no FBT is expected to be payable.

What’s Changed for FBT in 2026 and What the ATO is Focusing On

The 2026 FBT year feels different for many employers, not because the tax rates have changed, but because some important practical and legislative changes kicked in from 1 April 2025. As a result, FBT treatments that were correct last year may no longer apply, especially when it comes to vehicles and record keeping.

At the same time, the ATO has increased its compliance activity and data matching, meaning these changes are now actively enforced.

Below are the key changes from the last FBT year and how they align with the ATO’s current areas of focus.

-

The most significant change from the 2025 to 2026 FBT year is the removal of the FBT exemption for plug‑in hybrid electric vehicles (PHEVs).

From 1 April 2025, PHEVs are no longer treated as zero or low‑emission vehicles for FBT purposes. This means that, in the 2026 FBT year, new PHEV arrangements are subject to FBT, even where they would have been fully exempt in prior years.

A PHEV can only continue to be exempt where strict transitional conditions are met. These include that the vehicle was used or available for private use before 1 April 2025, a financially binding commitment was in place before that date, and the arrangement has not been varied, refinanced, extended, or changed since. Any change to the arrangement will generally cause the exemption to cease.

The ATO is actively reviewing PHEV arrangements in 2026, particularly where businesses have incorrectly assumed the exemption still applies.

-

Full electric vehicles and hydrogen fuel cell vehicles continue to qualify for the electric car FBT exemption in the 2026 FBT year, provided all eligibility conditions are met.

However, from the change in 2026, there is a higher level of scrutiny being applied. The ATO is checking that vehicles meet the luxury car tax threshold requirements, were first held and used within the required timeframes, and that exemptions are applied correctly under salary packaging and novated lease arrangements.

There is also increased focus on associated costs such as charging expenses, home charging calculations, and reportable fringe benefits reporting. Incorrect assumptions in these areas are now more likely to be identified.

-

One of the bigger changes for the 2026 FBT year is how record keeping works. The alternative record‑keeping rules have been around since 1 April 2024, but they are now very much part of how the ATO reviews FBT for the 2025 and later years. If you are relying on FBT exemptions or reductions, these records can now be considered as part of any ATO review.

Under these rules, employers can use existing business records instead of traditional travel diaries and some employee declarations for certain fringe benefits. The option applies on a benefit‑by‑benefit basis and was introduced through legislative instruments under the Fringe Benefits Tax Assessment Act 1986.

Depending on the benefit, acceptable alternative records may include:Employment contracts and job descriptions

Payroll and rostering records

Employer and employee correspondence, such as emails or text messages

Logbooks and internal policies

Hotel receipts, employee itineraries, and conference programs

Calculations showing private and business use

For the 2026 FBT year, the ATO is taking a much closer look at the alternative records employers are relying on. A common misunderstanding is thinking that if a formal declaration is no longer required, detailed evidence is no longer needed, but that is not how the ATO sees it. Alternative record keeping changes the format of the paperwork, not the level of proof required, and employers still need to clearly show how the taxable value was worked out and why an exemption or reduction applies

-

Entertainment continues to be a key risk area for FBT in the 2026 year, with the ATO applying closer scrutiny to how these costs are treated and reported. The change is not in the rules themselves, but in how actively the ATO is reviewing mismatches across income tax, GST, and FBT.

The ATO is focusing on situations where entertainment expenses are claimed as income tax deductions or GST credits, but no corresponding FBT has been returned. There is also increased attention on incorrect use of the minor benefits exemption and changes to entertainment valuation methods from one year to the next without a clear rationale.

Where entertainment costs appear in the accounts but no FBT return has been lodged, the ATO is now more likely to follow up. This makes accurate bookkeeping and a well‑structured chart of accounts critical for identifying and monitoring entertainment expenditure throughout the year.

The ATO continues to rely on TR 97/17 when determining whether food and drink constitutes entertainment, and businesses should ensure their treatment aligns with this guidance.

If you require assistance reviewing your entertainment treatment or setting up processes to accurately capture and assess entertainment expenditure, please contact us. -

Alongside these changes, the ATO has expanded its use of data matching across payroll systems, vehicle data, salary packaging providers, fuel cards, and employee contribution records.

This is a clear change from earlier years where FBT non‑compliance was often identified only through audits. In 2026, mismatches are more likely to be identified automatically, particularly where nil FBT returns are lodged despite benefits being provided.

FMA Partners is here to help

As the 2026 FBT year comes to a close, the key takeaway for businesses is that FBT compliance is less about new rules and more about taking the time to review existing arrangements. Vehicles, electric vehicles, entertainment, employee contributions and record keeping continue to be the main risk areas, and most issues arise from assumptions rather than intentional non‑compliance. An early review, supported by good records, can significantly reduce the risk of errors and ATO scrutiny.

At FMA Partners, we are here to help you navigate your FBT obligations and ensure your position is reviewed thoroughly and accurately. If you need any assistance or have questions about your FBT position, please do not hesitate to contact our office directly on 02 9540 6888 or via email at info@fmapartners.com.au.